This is what happens when the court looks at the timeline instead of just accepting the story.

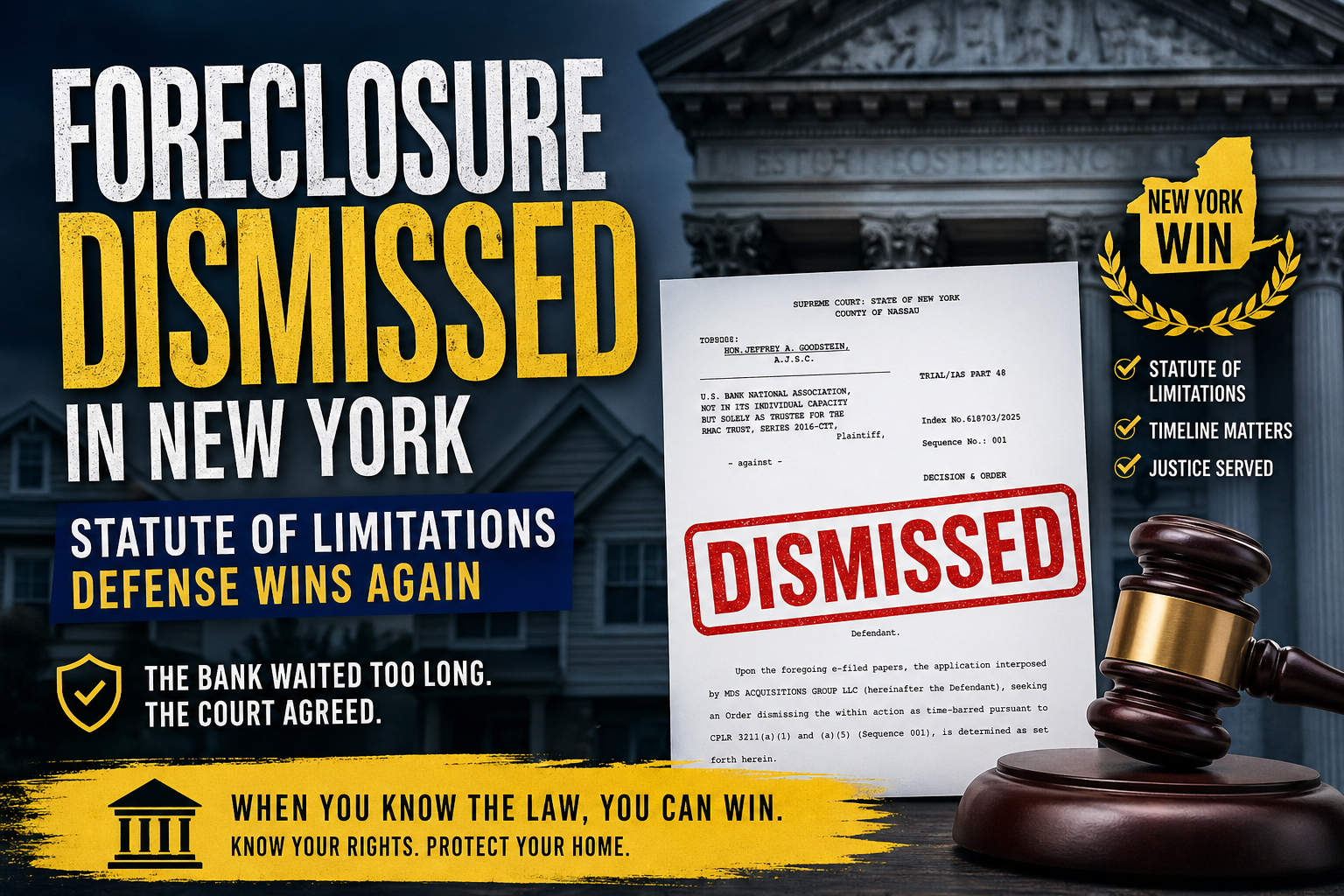

In a recent decision out of Nassau County, New York, the court dismissed a foreclosure action because it was filed too late. Not because of sympathy. Not because of technical tricks. But because the law was applied to the actual timeline. Our team at living lies was hired by a local NY attorney to do a case analysis and we’re proud to announce another win.

The statute of limitations had expired—and the bank could not fix it.

You can read the court’s decision here by subscribing to our private facebook group

The Case in Plain English

The loan in this case was originated back in 2009.

The borrower allegedly defaulted, and the first foreclosure action was filed in 2011. That matters. Because under New York law, that filing accelerated the debt.

Once that happened, the clock started.

And in New York, that clock is generally six years.

But here is where things get interesting.

Instead of resolving the case within that time frame, the foreclosure process dragged on. A second foreclosure action was filed in 2017. Then the case was discontinued. Later, another action was filed in federal court in 2019. That too was dismissed.

Finally, in 2025—more than a decade after the original acceleration—the bank tried again.

That was a problem.

What the Court Actually Found

The court did not guess. It did not assume. It followed the timeline.

According to the decision, the debt was accelerated when the first foreclosure action was filed in July 2011.

From that point forward, the six-year statute of limitations began to run on the entire debt.

And here is the key:

There was no valid de-acceleration.

The bank argued that a later loan modification in 2018 somehow reset the clock. But the court rejected that argument.

Why?

Because the modification occurred after the statute of limitations had already expired.

Once the claim is time-barred, you cannot revive it with a later document unless it meets very specific legal requirements.

This one did not.

The court also noted that there was no evidence of payments that would have restarted the clock under New York law.

So the conclusion was straightforward:

The action was untimely—and it had to be dismissed

We wrote about this very topic recently on our blog.

Learn more about the Statue of Limitations Defense here

This Is What We Mean by “Timeline Is Everything”

This case is a perfect example of something we have been saying for years:

Foreclosure cases are not just about documents. They are about chronology.

The bank had paperwork.

The bank had a story.

The bank had multiple bites at the apple.

But none of that mattered once the court focused on the timeline.

Once the debt was accelerated in 2011, the clock started running. And when that clock ran out, the case should have ended.

The problem for the bank is that it kept acting as if the clock did not exist.

The court disagreed.

Why the Loan Modification Did Not Save the Case

This is where many homeowners—and even some lawyers—get confused.

The bank argued that a 2018 loan modification somehow reset the statute of limitations.

That argument failed.

The court explained that once the statute of limitations has expired, you cannot simply revive the claim with a later agreement unless it meets strict requirements under New York law.

In this case, the modification was entered into after the six-year period had already run. That made it ineffective for reviving the claim. :contentReference[oaicite:4]{index=4}

This is critical.

Because homeowners are often told that modifications “fix everything.”

They do not.

And in some cases, they come too late to change the legal outcome.

What This Means for Homeowners

If you are facing foreclosure in New York—or anywhere else—you should take this seriously.

Do not assume the case is valid just because it was filed.

Do not assume the bank has unlimited time.

And do not assume that prior cases no longer matter.

In this case:

- The first foreclosure filing mattered

- The acceleration mattered

- The passage of time mattered

- The lack of de-acceleration mattered

- The lack of payments mattered

That is what won the case.

The Bigger Lesson

This is not about one case.

This is about a pattern.

Banks and servicers often assume that nobody will challenge the timeline. They assume that homeowners will focus on payments, hardship, or modification requests.

Meanwhile, the legal clock keeps running.

And sometimes, it runs out.

When that happens, the entire case can collapse.

This Is Why Evidence Beats Assumptions

This case was not won with slogans.

It was won with:

- dates,

- documents,

- procedural history, and

- application of the law to the timeline.

That is what courts are supposed to do.

And when they do it correctly, the result can be exactly what you see here:

Dismissal.

Conclusion

The statute of limitations is one of the most powerful defenses in foreclosure.

But it only works if you use it correctly.

You need to know when the debt was accelerated.

You need to know what happened in prior cases.

You need to know whether anything actually reset the clock.

And you need to prove it.

This New York decision shows exactly what happens when that work is done properly.

The case is dismissed.

Ask us how we helped win another case for homeowners facing an illegal foreclosure. Call us today at 866.216.4126 or submit your case statement here for a free consultation. And remember:

YOUR HOME IS YOUR CASTLE WE HELP YOU DEFEND IT

Internal Resources:

Frequently Asked Questions

Can a foreclosure be dismissed for being too old?

Yes. If the statute of limitations has expired, the case can be dismissed as time-barred.

Does a loan modification restart the statute of limitations?

Not necessarily. If the statute of limitations has already expired, a later modification may not revive the claim.

Why does acceleration matter?

Acceleration can trigger the start of the statute of limitations on the full debt, making it a critical issue in foreclosure cases.

Search Our Blog

Categories

Contact Our National Headquarters Phone: 844-583-5339

Connect with us

Contact Our National Headquarters

- 844-583-5339

- Available 24/7

-

200 S. Andrews Ave. Ste. 604

Ft. Lauderdale, FL 33301